Whether you have been told that you have a low credit score or you are simply curious about what yours is, you may be able to get an idea of your score by looking at the information you currently have. You can see how much you owe on your bills and how much credit you are using. You can also see your age and how much you have borrowed.

Age affects your credit score

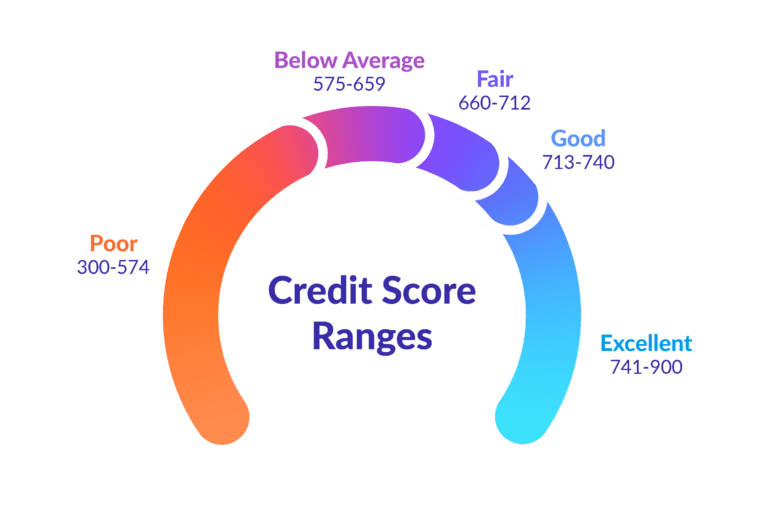

Having the right credit score can help you obtain lower interest rates, secure a better job, and more. Educating yourself on the various credit factors will help you avoid costly mistakes in the future.

Age is not considered a factor in credit scoring. However, some lenders may have limits on the amount of credit you can open. You can get a more detailed credit report from a credit rating agency. It will contain information on your loans, outstanding balances, and your credit score.

The FICO score, the score that most lenders will use to calculate your creditworthiness, is based on five factors. One of the more interesting is the length of your credit history. The longer the history, the better. You can also improve your score by making timely payments on your bills. However, if you want to increase your credit score, the best approach is to avoid opening too many credit cards.

While the average age of your accounts may not affect your score too much, the length of time that you have had any of those accounts will. You can calculate this by dividing the number of months that have passed since you opened a credit account by the total number of accounts. You may also want to consider adding an authorized user to one of your accounts. You should choose the oldest account possible.

The average credit card account has an age of about ten years. You may want to keep these accounts open for a while to build your credit history. The longest-lived account is also the sexiest, although it may come at the cost of having a high credit utilization rate.

A high credit utilization rate indicates that you may be in a financial crunch, and may be unable to afford a new credit card. This might lead to a lower credit score, but you might find it easier to obtain a loan with a better interest rate.

There are many factors that contribute to a credit score, but the average score varies from state to state. This is why it is important to know your credit score before you apply for a new loan.

Amounts Owed or Credit Utilization reveals how deeply in debt you are

Whether you are a credit card or a mortgage borrower, the Amounts Owed or Credit Utilization category is one of the most important categories to pay close attention to. This is because your monthly obligations will be affected by the amount you owe. For instance, you could be in for a rude awakening if you are carrying a high balance. Luckily, there are many tools to help you navigate this minefield.

One of the best ways to improve your FICO(r) score is to pay off your balances in full. You can do this by using cash or a debit card to make purchases. The best part is, you can use these cards again and again. As a result, your score will stay high for years to come. And, thanks to advances in online banking, your account balances will be updated in real time.

In fact, your score may even improve by as much as 15%. The Amounts Owed category is the linchpin of your FICO(r) score, making it one of the most important categories to address.

Applying for new credit affects your credit score

Using a new credit card can help your score if you use it responsibly. However, if you open a new credit card without paying on time, it can hurt your score. In fact, opening a new credit card can lead to late payments and may cause you to exceed your credit limit. This may send a message to your lender that you are a risky consumer.

A credit card’s length of history is also a factor in your score. If you have a long credit history, your score will be higher than someone with a shorter credit history. The average age of your accounts also plays a role. If your account is old, it will reflect negatively on your score.

If you have a low credit score, it is a good idea to have more than one credit card account. This will help your score and also give you a better mix of credit. However, applying for more than one card can also negatively affect your score.

Credit card applications are called “hard inquiries.” Hard inquiries stay on your credit report for two years. These inquiries have a small impact on your score. The impact is usually fewer than five points.

If you have a high credit score, the impact of a single credit card application may be minimal. If you have a lower score, a single card application may have a larger impact. Applying for more than six credit cards in a short period can cause a larger impact.

If you are planning to apply for a mortgage, opening a new credit card account can hurt your credit score. Your lender will check your credit to see if you qualify for a new mortgage. The amount of credit you get will also affect your credit score. If you are a new homebuyer, opening a credit card account can increase your debt-to-credit ratio. However, you may also be able to reduce your debt-to-credit ratio if you are approved for a balance transfer offer.

Using a new credit card responsibly can help your score recover. If you have a low credit score, it is best to apply for a new card when you are in a good position.

Paying down an installment loan favorably affects your credit score

Whether you are considering paying off an installment loan or simply trying to improve your credit, there are a few things you should know. Your credit score is a combination of your payment history, the length of your credit history, and how much debt you have. When you pay off debts on time, you will get a higher credit score. However, when you are late on a payment, you will see a lower credit score. Whether you are paying off a car loan or credit card, you should always pay on time.

Your credit utilization is another important factor that affects your credit score. Your credit utilization is the amount of your balance compared to the limit on your credit card. When you pay off an installment loan, your credit utilization will drop, and you will see a boost to your score.

While paying off an installment loan might seem like an easy way to boost your score, you should be careful about paying it off too early. This could hurt your credit. Also, avoid paying off an installment loan if you have other loans open. You might also be charged a prepayment penalty, which could make your payments more expensive.

Your mix of loans is also important to your credit score. Lenders want to see a diverse mix of accounts. This is particularly important when you are trying to get a new loan.

If you are looking to boost your score, it is important to choose a loan that offers favorable terms. You can also increase your credit score by keeping your credit card balances low. If you pay your credit card bills on time, you will see a steady increase in your credit score over time.

You should also be aware that a low credit utilization can make it harder to get new loans. Your credit score will also be negatively affected by a high number of revolving accounts. This is because revolving accounts do not disappear after you pay off your loan.

When you are trying to boost your credit, you can also look for installment loans that offer a lower interest rate. The length of the loan also has a big impact on the interest rate.